The Statistical Significance of Sessions in Bitcoin Trading

The Statistical Significance of Sessions in Bitcoin Trading

Sessions have individual characteristics. Different actors are active on the market at different times, leading to volume and volatility discrepancies and clear differences in market behavior. These differences have statistical significance.

Bitcoin charts with sessions highlighted (Exocharts)

To investigate this, we will pull the 1h OHLC Data of the Binance-Futures BTC pair from 2020 until 12/2024.

There are significant differences in proportions of dHigh and dLow distribution across sessions. This means that the sessions (Asia, London, and NY) exhibit statistically significant differences in their likelihood of containing the daily high or low. This can be observed running Cochran's Q test.

The distribution of daily highs/lows can be seen in the following table:

Table 1: Cochran's Q Test (High/Low)

The distribution of daily highs/lows can be seen in the following table. Note that pre-close accounts for New York, too. New York has by far the largest likelihood while Asia is in the second place and London is third by far (around half of Asia).

Table 2: Session Hit Rates

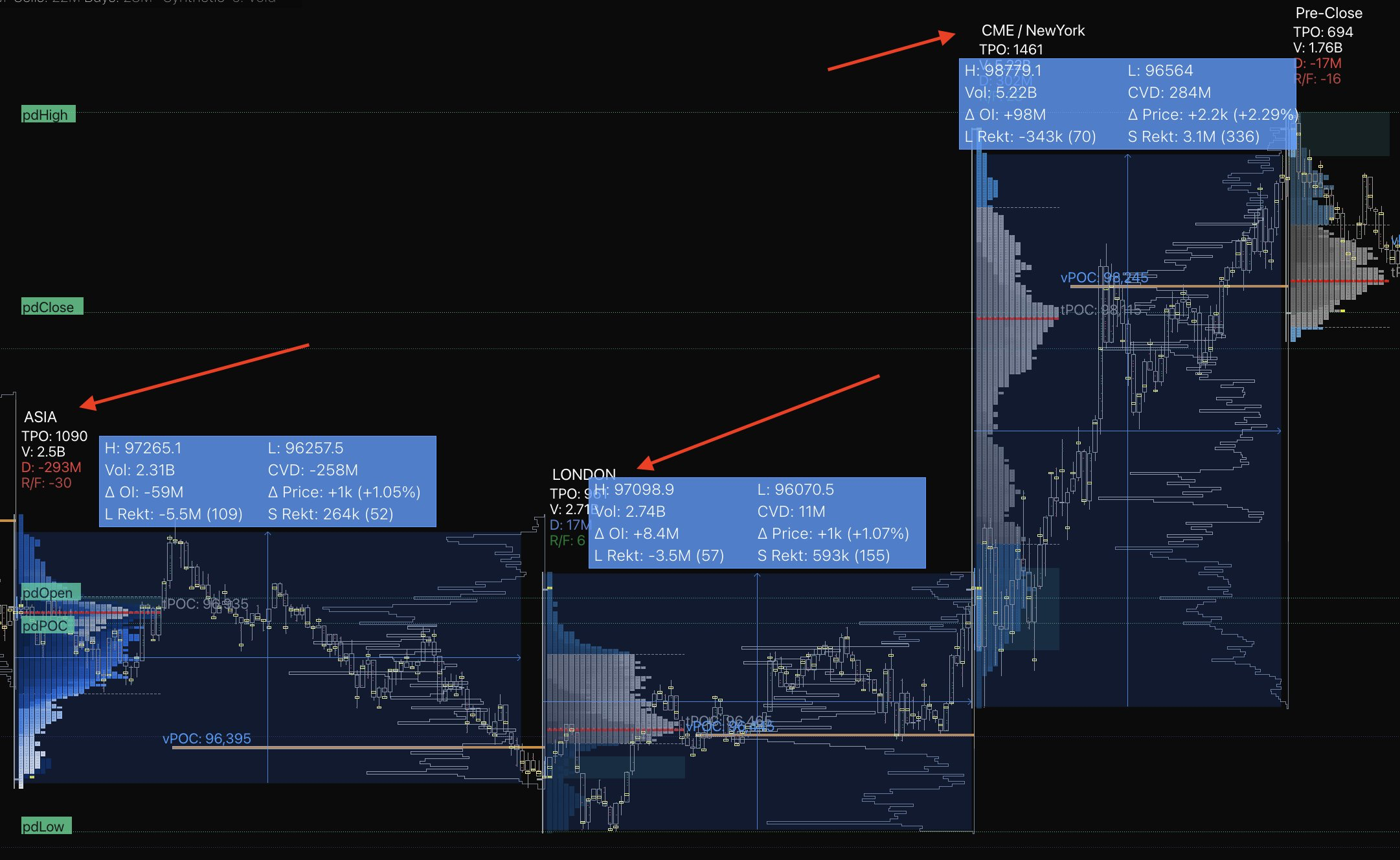

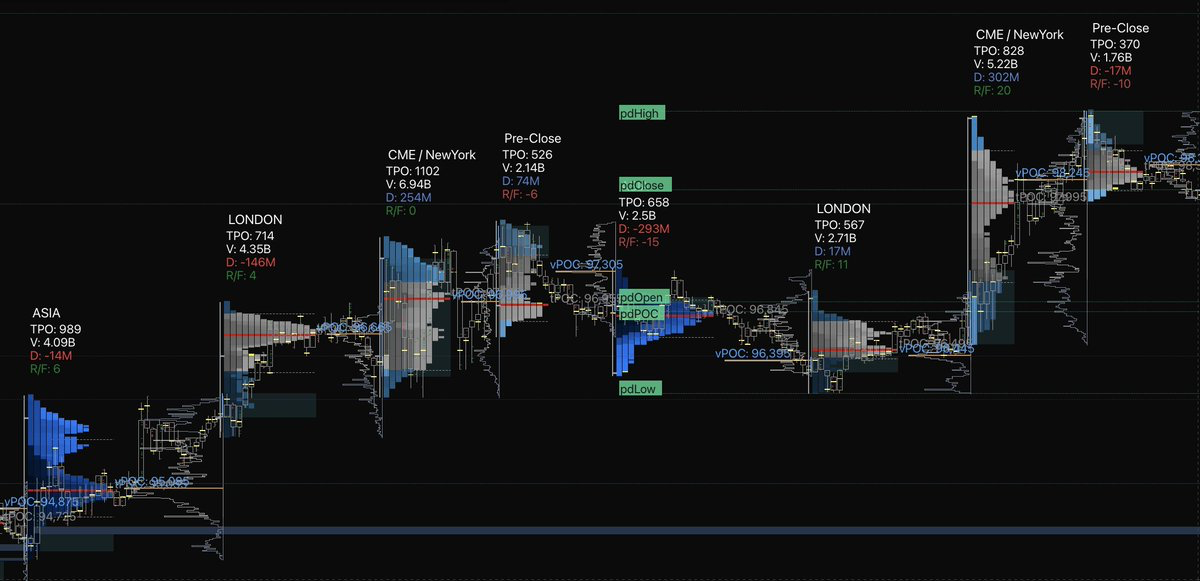

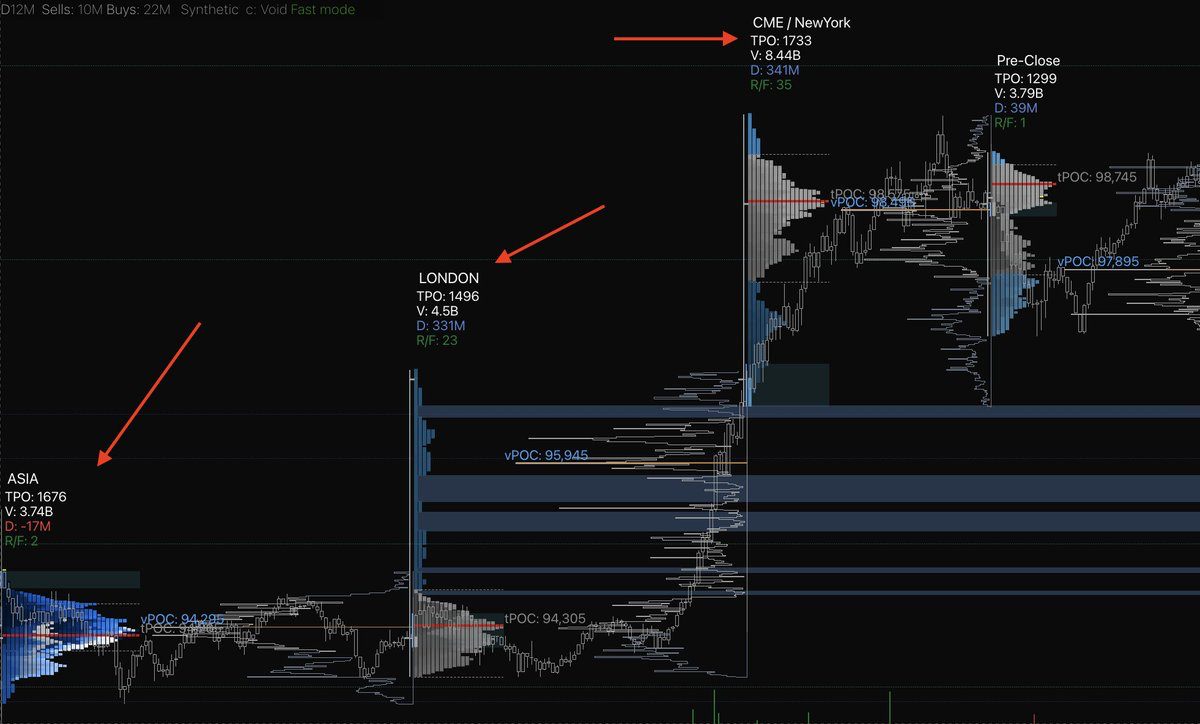

It can be easily observed on a chart that it is mostly NY putting in the highs/lows of the day.

Furthermore, there is significant variance in the likelihood of cross-session trend continuation. The NY & London sessions especially tend to follow the trend set by Asia (/London for NY).

Table 3: Trend Continuation Rates by Weekday and Session (Sorted)

This, too, is something that can be visually observed by looking through the Bitcoin chart.

It is quite easy to derive actionable trading insights from these observations. Of course, as with every single aspect, we must incorporate this knowledge into a wider system.